Apr

The Best Digital Wallets to Use in 2023: A Comprehensive Guide

In today’s rapidly evolving digital landscape, the use of digital wallets has emerged as a game-changer for various industries. With the convenience and security they offer, digital wallets are revolutionising the way businesses and consumers engage in financial transactions. According to the FIS Global Payments Report, digital wallet usage is projected to account for over half (52.5%) of global e-commerce transaction value by 2025, a significant increase from 48.6% in 2021. This growth is driven by the dominance of digital wallets in the Asia-Pacific region and the increasing adoption in other markets, including the United States and Europe.

The study also reveals the growing importance of digital wallets in various regions. In the United States, it is anticipated that one in three ecommerce payments will be made through digital wallets as they catch up to Asia-Pacific users. In Europe, digital wallets have already established themselves as the leading e-commerce payment channel, representing approximately 25% of the region’s transaction value in 2021.

As digital wallets become increasingly accessible through smartphones and mobile devices, the need for carrying physical cash or cards while traveling around is diminishing. The convenience of digital wallets allows users to make both online and offline payments with just a few clicks, streamlining the entire payment process and enhancing overall spending experiences. As the world embraces this transformative technology, digital wallets are sure poised to redefine the way we spend in our everyday lives in multiple industries globally.

With all that being said, it’s time to dive into The Best Digital Wallets to Use in 2023: A Comprehensive Guide!

Apple Pay

Apple Pay is a digital payment solution exclusive to Apple devices that allows users to make contactless payments. It can be used to pay for various goods and services in physical stores with NFC-enabled terminals or online through the Wallet app. The system is based on close-range data transmission using NFC technology and a Secure Element chip, which stores bank card data in encrypted form. The chip runs a Java application.

Source: Honest Pros and Cons

Advantages:

- Convenient – All operations are performed using a mobile device

- Budget tracking – Users can track all costs to optimise spending.

- Security – The service has a high level of security, making unauthorised access unlikely.

- Protection – If the device is lost, service data will be inaccessible to intruders.

Disadvantages:

- Limited to Apple devices – Apple Pay only works on Apple devices.

- Battery issues – Devices may run out of battery quickly.

- Performance – Older or refurbished models may experience system performance issues.

- Limited acceptance – Not all terminals are equipped with NFC technology for contactless payments.

Amazon Pay

Partner companies can add an Amazon Pay button on their websites, enabling customers to pay for goods and services. For stores, a fee of 2.9% of the transaction amount plus $0.3 applies, while international transactions are subject to a commission of 3.9% plus $0.3. To make a payment, customers can use their Amazon.com profile, with the service ensuring the security of all data.

SEPA payments are supported for European users, while SWIFT payments are available globally. Amazon also issues credit cards to regular customers, with no monthly fee required and a card delivered within a week of application. Payments can be made in the national currency and will be converted to US dollars at the average rate.

Source: Ecommerce Platforms

Advantages:

- Low transaction fees

- High level of security

- Quick and simple registration process

- No monthly service fee

Disadvantages:

- Integration with the store may take time

- No free trial available

- Customer support may take longer to process user requests

Dwolla

Dwolla is a payment system that offers low transaction fees, streamlined automation, and high-level security. It functions as an intermediary between banks and individuals/entrepreneurs and is particularly useful for bank transfers. To use the service, users need to create a personal account and link a bank account, which takes about 10 minutes. Funds are typically credited within one day.

Dwolla collaborates with many major US banks, including Bank of America and Silicon Valley Bank, which speaks to its reliability. The service offers three pricing plans: free/trial, standard, and corporate.

While Dwolla is most beneficial for US residents, users in other countries may face challenges when withdrawing funds. The transaction limit is $5,000 for the standard plan and $10,000 for the corporate plan, and the system only supports ACH payments – SEPA and SWIFT transfers are not possible. Additionally, Dwolla does not issue corporate or individual bank cards.

Source: Ecommerce Platforms

Advantages:

- Advanced features for developers

- Excellent technical support

- Fast payment processing

- “Virtual wallet” for sending, storing, and receiving funds

Disadvantages:

- High pricing for some tariff plans

- No credit card transactions

- Limited features for regular users

Cash App

Cash App, developed by Square Inc., is a peer-to-peer money transfer service that enables users to send and receive money, pay bills, and make purchases. Users can also obtain a debit card, the “Cash Card,” that allows them to use their Cash App balance to make purchases. Additionally, the app offers the ability to invest in stocks and buy/sell bitcoins.

Cash App has achieved a significant milestone in the adoption of Bitcoin payments and has become the most popular finance app in the US on the Google Play Store, surpassing PayPal in downloads. Originally launched in 2013 as Square Cash, the app has undergone minimal changes since its inception.

Source: LifeStyle

Advantages:

- Ability to buy and sell bitcoins directly from the Cash App balance

- High level of data protection with encryption and offline storage of bitcoins

Disadvantages

- Limited transparency for non-Bitcoin transactions on the app

- A 1.5% commission is charged for instant money transfers

- International digital payments are not supported

Samsung Wallet

Samsung is merging its Samsung Pay and Samsung Pass services into a new digital platform called Samsung Wallet, which will allow Galaxy device owners to securely manage their digital keys, boarding passes, ID cards, loyalty cards, and more in one mobile app. The platform promises defense-grade security through Samsung Knox, which is pre-installed on most Galaxy devices.

Advantages:

- Immediate activation and fast, secure online payments

- Rewarding application for users

Disadvantages:

- Limited to Samsung devices only

- Cannot be charged via ATMs, paychecks, or certain retail locations

Zelle

Zelle is an online platform for quickly sending and receiving money between US bank accounts. Zelle was designed by banks and made to be secure, using encryption to protect payment information. While Zelle does not protect against approved payments from fraud, they offer protection for unauthorised transactions, defined as transactions made without the account owner’s knowledge or consent. It is important to verify the recipient’s information before sending any payment to avoid potential fraud. Zelle is a free and easy-to-use application, and funds sent or received through Zelle are protected up to $250,000 per account.

Source: PC

Advantages:

- Allows quick and easy money transfers between US bank accounts

- Secure payment method that uses encryption to protect payment information

- Offers protection for unauthorized access or fraudulent activity, with a policy to refund victims through their bank

- Funds are protected up to $250,000 per account

Disadvantages:

- Does not protect approved payments from fraud

- No recourse if money is sent to the wrong person, as it is up to the recipient to return the funds

- Limited to use within the US and with participating banks only

Google Pay

Google Pay, also known as Android Pay, is a mobile application for the Android operating system that stores credit and debit cards in one place. The app ensures user data is safe within the digital wallet, and adding a card to the system is a quick and easy process. A user only needs to download the application to the device and select the desired card in the “Cards” tab.

Google Pay can be used at any location with a contactless payment terminal, allowing for use in almost all countries. The service charges a small fee to merchants for each payment, but there is no charge for maintaining or issuing a Google Wallet Card debit card. These cards are linked to the Google Pay system and allow users to withdraw cash from ATMs and pay for purchases in stores. However, the card is only valid for use within the United States.

Google Pay supports all possible currencies, but it is not suitable for international SWIFT payments or SEPA transfers.

Source: ink depot

Advantages:

- Conveniently stores credit and debit cards in one place

- User data is secure within the digital wallet

- Quick and easy setup process

- Can be used for in-store, online, and peer-to-peer payments

- Offers rewards and cashback for certain transactions

Disadvantages:

- Limited availability outside of Android devices

- Some merchants may not accept mobile payments

- No option to dispute unauthorised transactions within the app

- Some users have reported technical issues and glitches

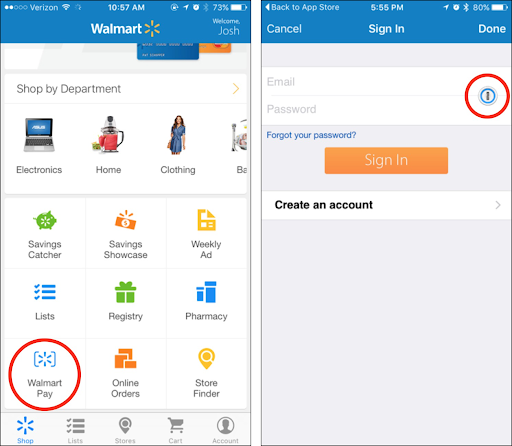

Walmart Pay

Walmart Pay uses QR codes generated by its app to allow users to pay for purchases without the need for an NFC-enabled mobile phone or credit/debit card. The payment system is compatible with all smartphones on the market, and any type of credit or debit card, including Walmart’s prepaid and gift cards, can be used to make purchases. The user simply needs to install the application on their device, and when they are ready to make a payment, they open the app, select Walmart Pay, and scan the QR code displayed by the checkout. Walmart Pay is a convenient and simple solution for customers who do not have access to newer mobile phones or NFC-enabled credit/debit cards.

Source: TidBits

Advantages:

- Compatible with all smartphones on the market

- Allows the use of any type of credit or debit card, as well as prepaid and gift cards

- No need for a new generation mobile phone with an NFC chip or any other advanced technology

- Quick and easy to use

- Provides an electronic receipt for purchases

- Can help users keep track of their spending

Disadvantages:

- Only available at Walmart stores

- QR codes can be slow to scan and may not work well in low-light conditions

- May not be as secure as other payment methods

- Requires users to have a Walmart account and link their payment method to it

- May not be as widely accepted as traditional credit or debit cards

PayPal

PayPal is a popular digital wallet that has been around since 1998, and it allows you to make online payments, send money to friends, and store funds from linked payment cards or bank accounts. Since its separation from eBay in 2015, PayPal has become an independent company, recognised by almost all countries, making it a convenient option for international purchases.

Source: startupguys

Advantages:

- Widely recognised by online stores worldwide

- Easy to register and use, even without a bank account

- Can link payment cards and bank accounts

- Able to send money to friends

- Works with 25 currencies

- Offers a high degree of protection for financial transactions

Disadvantages:

- Fees charged for certain types of transactions

- Some users report customer service issues

- Occasionally, account freezes or holds may occur if suspicious activity is detected

Venmo

Venmo is a mobile payment app owned by PayPal that allows users to instantly send and receive money. The service is promoted as safe, easy, and communicative, making it an excellent choice for sending money. Venmo is a consumer-friendly digital wallet app that emphasises social interaction. It is free and speedy, whether you want to pay for dinner with friends or share rent with a roommate. In addition, some small businesses use Venmo to accept payments. With 65 million users, Venmo is a popular and widely used payment platform.

Source: the ascent

Advantages:

- Instant and easy transfer of money

- Can be used for in-person and online purchases

- Social aspect allows for easy splitting of bills and expenses with friends

- No fees for standard transactions between Venmo accounts

- Can be used by small businesses to accept payments

Disadvantages:

- Limited buyer/seller protection for purchases made with Venmo

- Charges a fee for instant transfer of funds to a bank account

- Requires access to personal contacts and communication information

- May not be as widely accepted as other payment methods

- Potential for unauthorised transactions if account information is compromised.

Done By: Rejina Khar, Zarif Ong & Elly Ken

Source: Geniusee, Honest Pros and Cons, Ecommerce Platforms, LifeStyle, Android Authority, PC, InkDepot, TidBits, Startupguys, The Financial Brand & The Ascent